The solar industry is cutting how much silver goes into every panel as fast as it can, and the market is still headed for a sixth straight annual shortage.

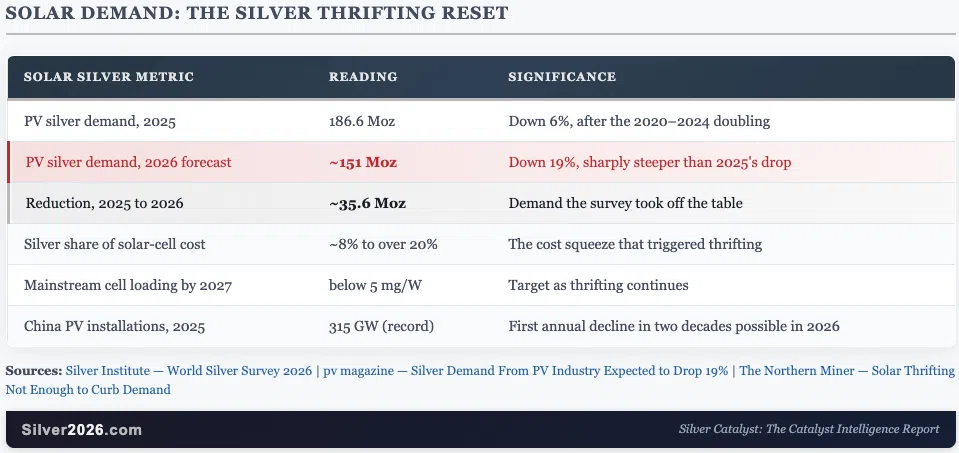

That is the tension worth understanding, because solar has been the single biggest growth engine in silver demand for half a decade, and the people who track the market just took a large slice of it off the table. Silver use in photovoltaics fell 6% in 2025 to 186.6 million ounces and is forecast to fall a further 19% in 2026 to roughly 151 million ounces, according to Metals Focus and the Silver Institute. For a metal whose bull case leans heavily on industrial demand, that is the kind of headline that should worry anyone who is long. It does not, and the reason is the whole point of this piece.

Silver trades around $68 an ounce as of June 18, modestly lower on the year after a volatile stretch. It dropped toward $68 in early June on strong economic data, bounced above $70 when the United States and Iran reached a deal to reopen the Strait of Hormuz, then slid again after the Federal Reserve signaled this week that its next move is more likely a rate hike than a cut. The macro tape has been loud. Underneath it, the demand map is quietly being redrawn, and solar is the loudest part of that story.

The research behind this issue comes from the Silver Engineer at Golden Meadow®, tracking more than a hundred separate forces that move the silver price. Solar is one of the most important and one of the most misread. A demand cut sounds bearish on its face. Whether it actually dents the structural shortage is a different question, and it turns on why the cut is happening.

There are five Deep Dives in this issue of the premium Silver Catalyst newsletter, and in this article, I'll focus on one of them: solar demand.

Solar Demand: Why Using Less Silver Doesn't Break the Case

Start with how big solar became. Between 2020 and 2024, silver use in solar panels more than doubled, from about 82 million ounces to roughly 197 million, as the world built renewable capacity at record pace. That made photovoltaics the largest single industrial use of silver and a major reason the market kept falling into deficit. So when that engine downshifts, it matters.

Here is what is actually happening. The silver price rose so far and so fast that silver's share of a solar cell's cost climbed from about 8% to more than 20%. At that level, manufacturers have every reason to use less, and they are. The industry calls it thrifting: refining how the silver paste is laid down and redesigning the cell so each panel needs less metal without losing performance. Newer techniques, including zero-busbar designs and ultra-fine printing, can cut silver per cell by another 10% to 20%, and mainstream cells are expected to fall below 5 milligrams of silver per watt by 2027. Some makers are going further and substituting copper outright.

The key fact for an investor is that this is a cut to silver per panel, not the end of solar. China installed a record 315 gigawatts of solar in 2025, and even though its market is expected to cool in 2026, possibly recording its first annual decline in two decades, the world is not going to stop building panels. What is happening is narrower than the headline. Thinner silver loadings per cell, together with somewhat softer installations this year, are pulling demand lower at the same time. But the metal is not being designed out of existence. It is being economized exactly where a high price pushes hardest.

There is also a floor under the substitution story. Copper electroplating and pure-copper pastes are advancing, but the reliability problems have not been solved, so mass production is not happening this year. The dominant cell technology, TOPCon, resists copper substitution because of how it is built, and silver stays essential in the highest-reliability applications. That is why analysts who follow the survey argue thrifting may not be enough to curb demand over time: the easy savings are being captured now, while the hard substitution still sits years out, and solar has a long build-out runway ahead, now reinforced by an energy-security case that has little to do with climate policy.

Sources: Silver Institute — World Silver Survey 2026 | pv magazine — Silver Demand From PV Industry Expected to Drop 19% | The Northern Miner — Solar Thrifting Not Enough to Curb Demand

What This Means to Silver Investors

A demand cut and a broken thesis are not the same thing. Solar silver demand is falling because the price did its job: it climbed high enough to force the biggest buyer to economize. That is normal price behavior, not a sign the metal is being replaced. The roughly 36 million ounces coming out of solar this year is real, and it is the honest bear case on silver. But it lands on a market that is still short.

Here is the part that matters. Even with that solar cut fully baked in, 2026 is on track for a sixth consecutive annual shortfall of about 46.3 million ounces, according to Metals Focus and the Silver Institute, the same structural gap I build the case around in Silver Rising. Total industrial silver demand is set to fall about 3% in 2026, and the market is in deficit anyway. That tells you how tight the underlying balance is: silver can lose its biggest growth engine to thrifting and still not have enough metal to go around.

It also frames the risk and the offset. The risk is that copper substitution arrives faster than expected and the thrifting curve keeps bending down. The offset is that thrifting has physical limits, copper is years from mass adoption in the dominant cell type, solar deployment has a long runway ahead, and the other big industrial uses, from grid build-out to electric vehicles to AI data centers, are growing while solar economizes. The way silver has traded throughout 2026, sliding from a January high above $121 to the high $60s while the deficit widened underneath, is a reminder that price and fundamentals can point in opposite directions for a while. The longer-term case rests on a shortage that a 19% solar cut did not close.

Solar is one dimension of the 100-catalyst framework I analyze in Silver Rising, alongside the four other Deep Dives in this issue of the Silver Catalyst newsletter. If you've at least considered investing in silver, I strongly encourage you to sign up, because it takes just $1 to get both. Get full Silver Catalyst Newsletter and Silver Rising book for $1 today.

Thank you.

The Silver Engineer